The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2 It’s Only Common Sense: Nice Guys Really Can Finish First

It’s Only Common Sense: Nice Guys Really Can Finish First The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin'Advanced Substrates: from FO to PCB

April 14, 2017 | Yole DéveloppementEstimated reading time: 2 minutes

As development of packaging technologies intensifies, in order to accommodate further front-end scaling trends and multi-die integration, advanced FO RDL and FC substrates represent the key interconnect components. The competition between FO and FC packages and the features of their interconnect components is resulting in an abundance of new package architectures that are crucial in enabling future products and markets. For this reason, the “More than Moore” market research and strategy consulting company Yole Développement (Yole) has established a stand-alone dedicated advanced substrate activity, focused on exploring the market, technologies and competition between thin film RDLs, and package substrates and its impact on PCBs.

The FO WLP platform is the advanced packaging platform with the highest growth, boasting revenue CAGRs of 49% from 2015 to 2021. The FO platform is forecasted to exceed US$2.5 billion in packaging services revenue by 2021.

In parallel FC packaging platform holds 85% of the advanced packaging market, but regardless of its solid 5% CAGR, it is losing market share to FO WLP resulting in a drop to 76% by 2021. The fast-rising FO WLP platform is ambitiously developing higher density solutions while at the same time facing more competition from advanced FC and hybrid FC solutions. Though the FC substrate market exhibited a dip in 2016 due to further adoption of FO lead by TSMC InFO, it is expected to bounce back with mild growth at a 1.6% revenue CAGR. This can be split into a 3.6% FC CSP CAGR and a stagnating 0.6% FC BGA CAGR. Overall, FC substrate revenue is expected to exceed US$8 billion by 2021.

Today’s advanced substrates in volume are FC substrates, 2.5D/3D TSV assemblies, and thin-film RDLs (FO WLP) below a L/S resolution of 15/15 um and with transition below L/S < 10/10 um. These interconnects are traditionally linked to higher-end logic (CPUs /GPUs , DSPs , etc.) driven by ICs in the latest technology nodes in the computing, networking, mobile, and high-end consumer market segments (gaming, HD /Smart TV). However, due to additional form factor and low power demands, WLP and advanced FC substrates are also widespread in majority of smartphone functions: application processors, baseband, transceivers, filters, amplifiers, WiFi modules, drivers, codecs, power management, etc.

Future higher-end products will require package substrates with L/S < 10/10 um and boards with L/S < 30/30 um. These demands have given rise to three distinct competition areas: Board vs. FC substrate FC substrate vs. FO WLP FO WLP vs. 2.5D/3D packaging.

The competitive areas of boards, substrates, and thin-film RDLs are directly linked to the underlying technologies used. Board manufacturers are representatives of the subtractive process, which is hard to scale beyond L/S 30/30 um. Meanwhile, substrate manufacturers have experience with SAP and mSAP processes that can lead to larger substrates and potentially “substrate-like PCBs”, but at higher cost. On the other side, when competing with FO WLP, FC substrates have a cost advantage but FO WLP scales faster.

Yole’s report compares the main processes and technologies used, discusses the limitations, advantages, and opportunities for each process, and provides roadmaps for thin-film RDLs (FO WLP) and FC substrates.

Furthermore, under this new report, Yole’s team proposes a common terminology for diverse substrate architectures and provides an advanced substrate segmentation, followed by in-depth analysis of advanced substrate drivers, markets and dynamics, the three competition areas, current and future FO and FC architectures, supply chain, player positioning, business model shifts, and advanced substrate market forecasts during the 2015 – 2021 period.

Share on:

Suggested Items

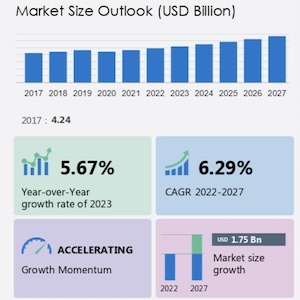

Industrial PC Market Size to Record $1.75 Billion Growth from 2023-2027

05/03/2024 | PRNewswireThe global industrial pc market size is estimated to grow by USD 1.75 billion from 2023 to 2027, according to Technavio. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of almost 6.29% during the forecast period.

Real Time with… IPC APEX EXPO 2024: Direct Imaging Equipment and Quad-wave DLP Light Engine Technology

05/03/2024 | Real Time with...IPC APEX EXPOGuest Editor Kelly Dack and MivaTek's Brendan Hogan delve into the company's innovative technologies, including direct imaging equipment and quad-wave DLP light engine technology. They highlight the benefits of direct imaging, compensation, and DART technology.

LQDX Divests Aluminum Soldering Business - Mina™ - to Taiyo America Inc.

05/02/2024 | PRNewswireLQDX, formerly known as Averatek Corp., developer of high-performance materials for advanced semiconductor manufacturing, today announced that it has divested its aluminum soldering business – known as MinaTM – to Taiyo America Inc., a global market leader in advanced electronic materials.

IDTechEx Report on Quantum Technology: Nano-scale Physics for Massive Market Impact

04/30/2024 | PRNewswireThe quantum technology market leverages nano-scale physics to create revolutionary new devices for computing, sensing, and communications. Across the industry, quantum technology offers a paradigm shift in performance compared with incumbent solutions.

Guerrilla RF Completes Strategic Acquisition of GaN Device Portfolio from Gallium Semiconductor

04/29/2024 | BUSINESS WIREGuerrilla RF, Inc. has finalized the acquisition of Gallium Semiconductor's entire portfolio of GaN power amplifiers and front-end modules. Effective April 26th, 2024, GUER acquired all previously released components as well as new cores under development at Gallium Semiconductor.