It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowTraditional PC Market Further Stabilizes as Top Companies Consolidate Share

October 11, 2017 | IDCEstimated reading time: 4 minutes

Worldwide shipments of traditional PCs (desktop, notebook, workstation) totaled 67.2 million units in the third quarter of 2017 (3Q17), which translates into a slight year-over-year decline of 0.5%, according to the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker. The results were better than projections of a 1.4% decline, and further demonstrate the trend of market stabilization in recent quarters. Improvement in emerging markets as well as back-to-school promotions helped boost results.

The component shortages of recent quarters have continued to improve and did not factor as a significant hindrance to production volumes. Nonetheless, higher component prices and inventory in some markets meant limited shipments and validated IDC assumptions about a muted third quarter. Not surprisingly, competitive pressures further cemented the dominance of the top five PC companies, which accounted for nearly 75% of the total traditional PC market.

From a geographic perspective, mature markets as well as emerging markets both struggled, with the notable exceptions of Japan and Canada, which continued to see positive growth in 3Q17, and Latin America, which rebounded after a dismal 2016 and first half of 2017.

"The traditional PC market performed much as expected in the third quarter," said Loren Loverde, program vice president, Worldwide PCD Trackers. "Emerging markets rebounded slightly more than anticipated, but overall results reflect the stabilization we expected following component and inventory adjustments. The outlook for the fourth quarter remains cautious, likely with a small decline in volume for the quarter and the year. The gains in emerging regions and potential for more commercial replacements represent some upside potential, although we continue to expect incremental declines in total shipments for the next few years."

"The U.S. traditional PC market exhibited lower overall growth, contracting 3.4% in 3Q17," said Neha Mahajan, senior. research analyst, Devices & Displays. "Despite the overall contraction, Chromebooks remain a source of optimism as the category gains momentum in sectors outside education, especially in retail and financial services."

Regional Highlights

United States: The U.S. traditional PC market experienced a fresh decline in shipments in 3Q17 with a notable drop in notebook sales. Continuing pressure from other mobile devices along with inventory management contributed to a drop in notebook shipments. Although, desktops did perform better than forecast, the category also experienced another declining quarter. Overall, total PC shipments for 3Q17 stood at 16.6 million units.

Europe, Middle East and Africa (EMEA): The EMEA traditional PC market continued to show clear signs of progress towards stabilization for another quarter. With customers increasingly adopting a mobility mindset, notebooks were undoubtedly the drivers for the EMEA PC market. Although desktops continued to erode, growing interest in gaming contributed towards keeping the desktop market afloat.

Asia/Pacific (excluding Japan): Traditional PC market results in Asia/Pacific (excluding Japan) came in close to expectations. China performed slightly better than anticipated following successful efforts of inventory clearing, which allowed for higher sell-in in the consumer and SMB segments. Shipments in India were supported by market recovery after the GST reform, while the education sector benefited from roll out of the ELCOT project.

Japan: The Japan traditional PC market showed stable growth in 3Q17, primarily driven by refresh projects and migration to Windows 10 as well as further notebook adoption. As a result, the year-over-year growth of the overall Japan traditional PC market will be in line with forecast.

Company Highlights

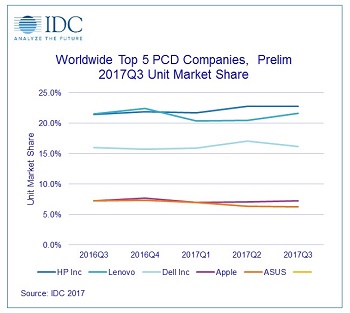

HP Inc. retained the top spot and further lengthened its lead with nearly 23% share of the market, helped in part by major wins in Asia/Pacific. HP was the only top vendor to manage a notable shipment increase with growth of 6% on the year.

Lenovo held the second position with volume holding flat at 0.1% year-over-year growth. The company continued to struggle in North America, with weak notebook sales, but also seemed to have slowed its recent decline in Asia/Pacific.

Dell remained in the third position, and grew 0.8% year over year. Dell fared well internationally, but saw declining volume in North America.

Apple kept the fourth position, keeping shipments roughly flat with growth of 0.3% year over year.

ASUS retained the fifth position, but was the only company in the top 5 to decline faster than the market average.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, company share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC's Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of International Data Group (IDG), the world's leading media, data and marketing services company that activates and engages the most influential technology buyers.

Share on:

Suggested Items

Orbex Secures £16.7m Investment for Rocket ‘Ramp Up’ Period

04/24/2024 | OrbexThe UK spaceflight company Orbex has received £16.7m from six backers in an update to its Series C funding round.

Real Time with... IPC APEX EXPO 2024: Going Vertical: SCHMID's Advanced Solutions for Printed Circuit Boards

04/24/2024 | Real Time with...IPC APEX EXPOEditor Marcy LaRont chats with Bob Ferguson, the president of SCHMID, about advanced solutions for PCBs and the equipment they are highlighting at this year's show. He delves into vertical no-touch handling systems and the prospect of achieving sub-10-micron lines. Inspired by SCHMID's technology, Bob expresses excitement about where the industry is today.

Real Time with... IPC APEX EXPO 2024: Advancements in Laser Depaneling with LPKF

04/24/2024 | Real Time with...IPC APEX EXPOJake Benz, LPKF sales manager for North America, discusses the company's advancements in laser depaneling. LPKF has introduced a green wavelength laser for processing rigid FR-4 circuit boards, bringing significant gains in processing speeds to market. The company transitioned from IR CO2 to UV wavelength due to heat and burning issues.

Adura Solutions Exhibits at Del Mar 2024

04/24/2024 | Adura SolutionsSumit Tomar, CEO of Adura Solutions, has announced that his company will be exhibiting at this year’s Del Mar Electronics and Manufacturing Show to be held at the Del Mar Fairgrounds, San Diego, California, April 24-25.

Winner of The Science Show Rakett 69 Receives Incap Scholarship

04/24/2024 | IncapThe winner of the Rakett 69 science show, Andri Türkson, who stood out as an electronics enthusiast, received a scholarship from Incap Estonia, along with an internship opportunity in Saaremaa.