Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024

It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024 Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowEurozone Economic Growth Remains Solid in April

May 7, 2018 | IHS MarkitEstimated reading time: 6 minutes

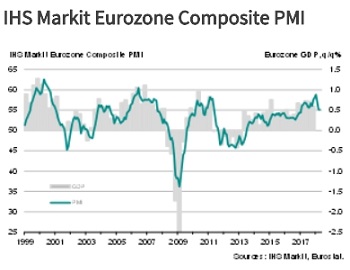

Eurozone economic activity continued to expand at a robust pace in April, with solid growth signalled in both the manufacturing and service sectors. However, growth has downshifted in recent months. The latest expansion of output was the slowest since January 2017.

The final IHS Markit Eurozone PMI Composite Output Index posted 55.1 in April, down from 55.2 in March and below the earlier flash estimate (also 55.2). The headline index has signalled expansion in each of the past 58 months and remains above its average for that sequence (54.0). April saw manufacturing production rise at a marginally quicker pace, but this was offset by growth in service sector activity easing to an eight-month low.

Ireland rose back to the top of the PMI output growth table in April, with its rate of expansion hitting a three-month high. France also registered faster growth (a two-month high). The other nations covered reported further slowing in their rates of expansion, to a 19-month low in Germany, a 15-month low in Italy and a four-month low in Spain.

The weaker growth of eurozone economic output reflected a tandem slowdown in the rate of expansion in incoming new business. New orders rose at the slowest, albeit still solid, pace for 15 months. Growth eased in both the manufacturing (17-month low) and service (eight-month low) sectors.

Intakes of new work were still sufficiently robust to test capacity, as indicated by a further rise in outstanding business in April. This encouraged companies to expand employment, with job creation registered for the forty-second month in a row. The pace of growth also ticked higher and remained among the best seen over the past decade.

Employment increased in all of the nations covered, with only Spain failing to see a faster rate of increase. The strongest rises were reported in Ireland, Germany and France.

Price pressures continued to moderate in April, with rates of increase in input costs and output charges easing to seven- and four-month lows respectively. Input price increases remained elevated nonetheless, reflecting high raw material costs (often due to demand exceeding supply) and growing staff costs.

Services

The final IHS Markit Eurozone PMI Services Business Activity Index fell to an eight-month low of 54.7 in April, down from 54.9 in March and below the earlier flash estimate of 55.0. The index remained at a level consistent with solid expansion and above its long-run average (53.2).

The upturn remained broad-based in April, with activity rising across all of the nations covered. Ireland and France registered the strongest increases and were the only countries to see faster rates of growth. Output rose at slower rates in Germany (19-month low) and Spain (four-month low) and steadied at March’s five-month low in Italy.

A similar easing was seen in the rate of increase of new orders at euro area service providers, which was also at an eight-month low in April. This was still sufficient to test capacity, as backlogs of work rose for the twenty-third straight month (albeit at a weaker pace).

Companies responded to the continued growth in both new business and backlogs of work by increasing employment. The pace of job creation was the fastest since October 2007. Rates of increase improved in Germany (three-month high), France (two-month high), Italy (four-month high) and Ireland (four-month high), but eased to a 14-month low in Spain.

April saw input price inflation accelerate for the first time since January. However, the rate of increase remained well below January’s near seven-year high. In contrast, output charges rose at the slowest pace in seven months.

The outlook for the eurozone service sector remained positive in April, although the degree of optimism eased to a four-month low. Business confidence improved in Spain and Ireland, was unchanged in France and eased slightly in Germany and Italy.

Chris Williamson, Chief Business Economist at IHS Markit, said:

“The final PMI numbers confirm the marked, broad-based fading of the eurozone’s growth spurt so far this year. The headline index has fallen from an eleven-and-a-half year peak in January to a 15-month low in April. Despite the drop, the PMI is not yet at a worryingly low level, but the survey details hint at further easing in the coming months.

“While the expansion signalled by April’s PMI is disappointing relative to the elevated levels seen at the start of the year, the survey remains indicative of the eurozone economy growing at a robust quarterly rate of approximately 0.5-0.6%. Employment growth is also still booming, with the rate of job creation in the service sector at its highest for over a decade.

“Employment is a lagging indicator, however, and two reliable leading indicators have turned down, suggesting that both output and hiring trends will weaken further, at least into May. First, backlogs of uncompleted orders grew at the slowest rate for eight months. Second, companies’ expectations about future output hit a five-month low. Any further deterioration could herald new concerns among policymakers regarding the economic outlook.”

The Eurozone Composite PMI (Purchasing Managers' Index) is produced by IHS Markit and is based on original survey data collected from a representative panel of around 5,000 manufacturing and services firms. National manufacturing data are included for Germany, France, Italy, Spain, the Netherlands, Austria, the Republic of Ireland and Greece. National services data are included for Germany, France, Italy, Spain and the Republic of Ireland.

The Eurozone Services PMI (Purchasing Managers' Index) is produced by IHS Markit and is based on original survey data collected from a representative panel of around 2,000 private service sector firms. National data are included for Germany, France, Italy, Spain and the Republic of Ireland. These countries together account for an estimated 78% of eurozone private sector services output.

The final Eurozone Composite PMI and Services PMI follows on from the flash estimate which is released a week earlier and is typically based on approximately 75%–85% of total PMI survey responses each month. The April composite flash was based on 85% of the replies used in the final data. The April services flash was based on 79% of the replies used in the final data. Data were collected 12-25 April.

The average differences between the flash and final PMI index values (final minus flash) since comparisons were first available in January 2006 are as follows (differences in absolute terms provide the better indication of true variation while average differences provide a better indication of any bias):

The Purchasing Managers’ Index (PMI) survey methodology has developed an outstanding reputation for providing the most up-to-date possible indication of what is really happening in the private sector economy by tracking variables such as sales, employment, inventories and prices. The indices are widely used by businesses, governments and economic analysts in financial institutions to help better understand business conditions and guide corporate and investment strategy. In particular, central banks in many countries (including the European Central Bank) use the data to help make interest rate decisions. PMI surveys are the first indicators of economic conditions published each month and are therefore available well ahead of comparable data produced by government bodies.

About IHS Markit

IHS Markit is a world leader in critical information, analytics and expertise to forge solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 key business and government customers, including 85 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

About PMI

Purchasing Managers’ Index (PMI) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely-watched business surveys in the world, favoured by central banks, financial markets and business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends.

Share on:

Suggested Items

D Coupon Testing and Data Insights With GreenSource Fabrication

04/17/2024 | Marcy LaRont, PCB007 MagazineMarcy LaRont spoke with Steve Karas of GreenSource Fabrication at the SMTA UHDI conference in March. He presented a case study that GreenSource undertook with a customer on critical via reliability with advanced materials and used the experience to highlight the importance and effectiveness of D coupon testing. He also discussed GreenSource’s approach to data aggregation and a new system they developed to use collected data effectively.

Real Time with... IPC APEX EXPO 2024: Innovations in Thermal, Warpage, and Strain Metrology

04/17/2024 | Real Time with...IPC APEX EXPOEditor Nolan Johnson talks with Neil Hubble, president of Akrometrix, about the company's leadership in thermal, warpage, and strain metrology. Neil details how Akrometrix is committed to addressing customer challenges through technological evolution, innovative solutions, and a focus on data processing. A tabletop unit for thermal warpage testing is showcased at IPC APEX EXPO this year.

Signal Integrity Expert Donald Telian to Teach 'Signal Integrity, In Practice' Masterclass Globally

04/17/2024 | PRLOGDonald Telian and The EEcosystem announce the global tour of "Signal Integrity, In Practice," a groundbreaking LIVE masterclass designed to equip hardware engineers with essential skills for solving Signal Integrity (SI) challenges in today's fast-paced technological landscape.

SMT Prospects and Perspectives: AI Opportunities, Challenges, and Possibilities, Part 1

04/17/2024 | Dr. Jennie Hwang -- Column: SMT Perspectives and ProspectsIn this installment of my artificial intelligence (AI) series, I will touch on the key foundational technologies that propel and drive the development and deployment of AI, with special consideration of electronics packaging and assembly.

Argonne, RIKEN Sign a Memorandum of Understanding in Support of AI for Science

04/16/2024 | BUSINESS WIRELeaders in high performance computing in the U.S. and Japan have signed a memorandum of understanding (MOU) establishing a cooperative relationship in support of artificial intelligence (AI) computing projects.