It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowDRAM Market Braces for Slower Growth

October 8, 2018 | IC InsightsEstimated reading time: 2 minutes

History suggests that DRAM ASP and market growth will soon trend downward; suppliers cautious and stand ready to adjust capex expansion plans.

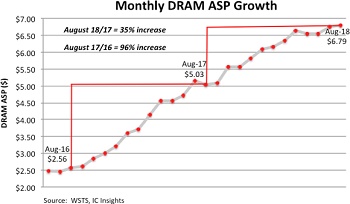

In its September Update to The 2018 McClean Report, IC Insights discloses that over the past two years, DRAM manufacturers have been operating their memory fabs at nearly full capacity, which has resulted in steadily increasing DRAM prices and sizable profits for suppliers along the way. The DRAM average selling price (ASP) reached $6.79 in August 2018, a 165% increase from two years earlier in August of 2016. Although the DRAM ASP growth rate has slowed this year compared to last, it has remained on a solid upward trajectory through the first eight months of 2018.

The DRAM market is known for being very cyclical and after experiencing strong gains for two years, historical precedence now strongly suggests that the DRAM ASP (and market) will soon begin trending downward. One indicator suggesting that the DRAM ASP is on the verge of decline is back-to-back years of huge increases in DRAM capital spending to expand or add new fab capacity. DRAM capital spending jumped 81% to $16.3 billion in 2017 and is expected to climb another 40% to $22.9 billion this year. Capex spending at these levels would normally lead to an overwhelming flood of new capacity and a subsequent rapid decline in prices.

However, what is slightly different this time around is that big productivity gains normally associated with significant spending upgrades are much less at the sub-20nm process node now being used by the top DRAM suppliers as compared to the gains seen in previous generations.

At its Analyst Day event held earlier this year, Micron presented figures showing that manufacturing DRAM at the sub-20nm node requires a 35% increase in the number of mask levels, a 110% increase in the number of non-lithography steps per critical mask level, and 80% more cleanroom space per wafer out since more equipment—each piece with a larger footprint than its previous generation—is required to fabricate ≤20nm devices. Bit volume increases that previously averaged around 50% following the transition to a smaller technology node, are a fraction of that amount at the ≤20nm node. The net result is suppliers must invest much more money for a smaller increase in bit volume output. So, the recent uptick in capital spending, while extraordinary, may not result in a similar amount of excess capacity, as has been the case in the past.

The DRAM ASP is forecast to rise 38% in 2018 to $6.65, but IC Insights forecasts that DRAM market growth will cool as additional capacity is brought online and supply constraints begin to ease. (It is worth mentioning that Samsung and SK Hynix in 3Q18 reportedly deferred some of their expansion plans in light of expected softening in customer demand.)

Of course, a wildcard in the DRAM market is the role and impact that the startup Chinese companies will have over the next few years. It is estimated that China accounts for approximately 40% of the DRAM market and approximately 35% of the flash memory market.

At least two Chinese IC suppliers, Innotron and JHICC, are set to participate in this year’s DRAM market. Although China’s capacity and manufacturing processes will not initially rival those from Samsung, SK Hynix, or Micron, it will be interesting to see how well the country’s startup companies perform and whether they will exist to serve China’s national interests only or if they will expand to serve global needs.

Share on:

Suggested Items

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.

Real Time with... IPC APEX EXPO 2024: Exploring Silicone Solutions with R&D Director of CHT

04/17/2024 | Real Time with...IPC APEX EXPOIn this interview, Gerry Ellis, the R&D director for CHT, discusses the product range offered by his company. He explains the challenges in creating base formulations, the drive to make products more user-friendly, and the various application techniques involved. Ellis also highlights the key market segments and the significance of providing efficient solutions to customers.