The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustrySmartphone Shipment Down 5% in 4Q18

January 31, 2019 | IDCEstimated reading time: 5 minutes

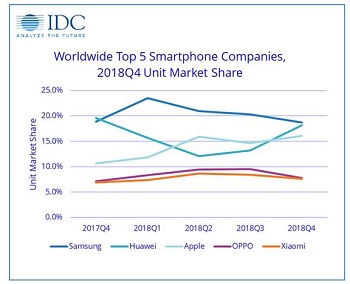

According to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, smartphone vendors shipped a total of 375.4 million units during the fourth quarter of 2018 (4Q18), down 4.9% year over year and the fifth consecutive quarter of decline. The challenging holiday quarter closes out the worst year ever for smartphone shipments with global smartphone volumes declining 4.1% in 2018 with a total of 1.4 billion units shipped for the full year. With challenging market conditions continuing into the first quarter of 2019, the likelihood of a declining market this year becomes more of a reality.

"Globally the smartphone market is a mess right now," said Ryan Reith, program vice president with IDC's Worldwide Mobile Device Trackers. "Outside of a handful of high-growth markets like India, Indonesia, Korea, and Vietnam, we did not see a lot of positive activity in 2018. We believe several factors are at play here, including lengthening replacement cycles, increasing penetration levels in many large markets, political and economic uncertainty, and growing consumer frustration around continuously rising price points."

Despite all the challenges the smartphone market is facing, the largest focal point remains the China market as recovery continues to get pushed further forward. China, which accounts for roughly 30% of the world's smartphone consumption, had an even worse 2018 than the previous year with volumes down just over 10%. High inventory continues to be a challenge across the market as is consumer spending on devices, which has been down overall. At the same time the top 4 brands, all of which are Chinese—Huawei, OPPO, vivo, and Xiaomi—grew their share of the China market to roughly 78%, up from 66% in 2017.

On a worldwide basis, the top 5 smartphone companies continue to get stronger and now account for 69% of smartphone volume, up from 63% a year ago. If vivo is included, which is currently number six and has been in and out of the top 5 in recent quarters, the share of the top companies is 75% and growing. While the market faces some very serious challenges in general, none are greater than the challenges facing the brands that continue to lose market share and channel positioning.

"With replacement rates continuing to slow across numerous markets, vendors will need to find a new equilibrium that balances the latest smartphone features, compelling design, and affordability," said Anthony Scarsella, research manager with IDC's Worldwide Quarterly Mobile Phone Tracker. "The arrival of both 5G and foldable devices later this year could bring new life to the industry depending on how vendors and carriers market the real-life benefits of these technologies. However, we expect these new devices to elevate average selling prices as new displays, chipsets, and radios will bring an increased price to the BOM (build of materials), which will translate to higher price points for consumers. To combat this, carriers and retailers will need to fully maximize trade-in offers for older devices as a type of subsidy to push upgrades throughout 2019."

Page 1 of 2

Share on:

Suggested Items

Warm Windows and Streamlined Skin Patches – IDTechEx Explores Flexible and Printed Electronics

04/26/2024 | IDTechExFlexible and printed electronics can be integrated into cars and homes to create modern aesthetics that are beneficial and easy to use. From luminous car controls to food labels that communicate the quality of food, the uses of this technology are endless and can upgrade many areas of everyday life.

iNEMI Packaging Tech Topic Series: Role of EDA in Advanced Semiconductor Packaging

04/26/2024 | iNEMIAdvanced semiconductor packaging with heterogenous integration has made on-package integration of multiple chips a crucial part of finding alternatives to transistor scaling. Historically, EDA tools for front-end and back-end design have evolved separately; however, design complexity and the increased number of die-to-die or die-to-substrate interconnections has led to the need for EDA tools that can support integration of overall design planning, implementation, and system analysis in a single cockpit.

Koh Young Showcases Award-winning Inspection Solutions at SMTconnect with SmartRep in Hall 4A.225

04/25/2024 | Koh Young TechnologyKoh Young Technology, the industry leader in True 3D measurement-based inspection solutions, will showcase an array of award-winning inspection and measurement solutions at SMTconnect alongside its sales partner, SmartRep, in booth 4A.225 at NürnbergMesse from June 11-13, 2023. The following offers a glimpse into what Koh Young will present at the tradeshow:

Real Time with… IPC APEX EXPO 2024: Plasmatreat: Innovative Surface Preparation Solutions

04/25/2024 | Real Time with...IPC APEX EXPOIn this interview, Editor Nolan Johnson speaks with Hardev Grewal, CEO and president of Plasmatreat, a developer of atmospheric plasma solutions. Plasmatreat uses clean compressed air and electricity to create plasma, offering environmentally friendly methods for surface preparation. Their technology measures plasma density for process optimization and can remove organic micro-contamination. Nolan and Hardev also discuss REDOX-Tool, a new technology for removing metal oxides.

Nanotechnology Market to Surpass $53.51 Billion by 2031

04/25/2024 | PRNewswireSkyQuest projects that the nanotechnology market will attain a value of USD 53.51 billion by 2031, with a CAGR of 36.4% over the forecast period (2024-2031).