It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowSemiconductor R&D Spending Will Step Up After Slowing

February 1, 2019 | IC InsightsEstimated reading time: 2 minutes

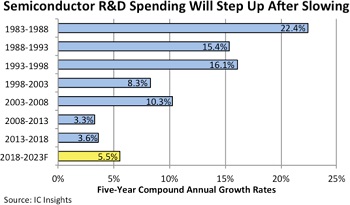

3D die-stacking technologies, manufacturing barriers, and growing complexities in end-use systems are among the technical challenges that are expected to lift R&D growth rates through 2023.

The semiconductor business is defined by rapid technological changes and the need to maintain high levels of investment in research and development for new materials, innovative manufacturing processes for increasingly complex chip designs, and advanced IC packaging technologies.

However, since the 1980s, the long-term trend has been toward a slowdown in the annual growth rate of research and development expenditures according to data presented in the new, 2019 edition of IC Insights’ McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry (released in January 2019). Consolidation in the semiconductor industry has been a big factor contributing to lower growth rates for R&D expenditures so far this decade. In the most recent five-year span from 2013-2018, semiconductor R&D spending grew by CAGR of 3.6% per year, essentially unchanged from the 3.3% experienced from 2008-2013.

IC Insights expects new challenges such as three-dimensional (3D) die-stacking technologies, growing complexities in end-use applications, and other significant manufacturing barriers to raise semiconductor R&D spending to a slightly higher growth rate of 5.5% per year in the 2018-2023 forecast period.

R&D spending trends discussed here cover expenditures by integrated device manufacturers (IDMs), fabless chip suppliers, and pure-play wafer foundries and do not include other companies and organizations involved in semiconductor-related technologies, such as production equipment and materials suppliers, packaging and test service providers, universities, government-funded labs, and industry cooperatives, such as IMEC in Belgium, the CAE-Leti Institute in France, the Industrial Technology Research Institute (ITRI) in Taiwan, and the U.S.-based Sematech consortium, which was merged into the State University of New York (SUNY) Polytechnic Institute in 2015.

With the value of more than 90 merger and acquisition agreements topping $250 billion since 2015, tremendous consolidation has been underway among semiconductor suppliers—many of them major IC companies—which have been cutting costs by hundreds of millions of dollars and leveraging “synergies,” meaning the elimination of overlapping expenditures (e.g., jobs, facilities, and R&D activities) in an attempt to achieve higher levels of productivity and greater profits. After rising just 1% in 2015 and 2016, total semiconductor R&D spending grew 6% in 2017 and increased 7% in 2018 to reach a new record- high level of $64.6 billion.

During the last 40 years (1978-2018), R&D expenditures have increased at a compound annual growth rate of 14.5%, slightly higher than the total semiconductor revenue CAGR of 12.0%. Since the year 2000, semiconductor R&D spending as a percent of worldwide sales has exceeded the 40-year historical average of 14.5% in all but four years (2000, 2010, 2017, and 2018). In these four years, lower R&D-to-sales ratios had more to do with the strength of revenue growth than weakness in research and development spending.

Share on:

Suggested Items

GlobalFoundries Commits to Achieving Net Zero Emissions and Carbon-Neutral Power by 2050

04/23/2024 | GlobalFoundriesGlobalFoundries (GF) is furthering its commitment to sustainable operations and fighting climate change with the announcement of two new long-term goals to achieve net-zero greenhouse gas (GHG) emissions and 100% carbon-neutral power by 2050.

ROHM Group Company SiCrystal and STMicroelectronics Expand Silicon Carbide Wafer Supply Agreement

04/23/2024 | ROHMROHM and STMicroelectronics, a global semiconductor leader serving customers across the spectrum of electronics applications, announced today the expansion of the existing multi-year, long-term 150mm silicon carbide (SiC) substrate wafers supply agreement with SiCrystal, a ROHM group company.

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.

Altus Group Helps BitBox Unlock Productivity and Efficiency Gains with New Reflow Oven

04/22/2024 | Altus GroupAltus Group, a leading provider of capital equipment, has recently assisted BitBox, a UK-based electronics design, engineering and manufacturing company in upgrading its operations with the implementation of a new reflow oven from Heller Industries.

Growth Potential: Electronics Manufacturing Driving Massive Surge in Manufacturing Investment

04/22/2024 | Shawn DuBravac, IPCIn the early months of the pandemic, investment in manufacturing infrastructure, such as plants and production facilities, declined sharply. Real investment dropped over 11%, before finally recovering to pre-pandemic levels in the first half of 2022. Over the past two years, however, several factors have combined to drive manufacturing investment to record levels.