It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowSupply Chain, Geopolitical Issues to Stem Commercial Appetite Growth of EMEA PC Market in 2019

February 27, 2019 | IDCEstimated reading time: 2 minutes

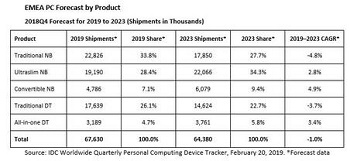

EMEA shipments of traditional PCs (a combination of desktops, notebooks, and workstations) will total 67.6 million in 2019, a 3.5% YoY decline, according to IDC's latest Quarterly PCD Tracker. Ongoing renewals and the impending end of Windows 7 support will provide plenty of units for the commercial segment to remain afloat, but this will be insufficient to offset the heavy decline in the consumer space. Ultramobile devices will continue to fare far better than their traditional counterparts, with ultraslims expected to continue on their strong growth trajectory across both segment groups.

Accelerating demand for mobility to address the growing prevalence of mobile workers, combined with the imminent end of Windows 7 support, now just a year away, will incentivize notebook refreshes in both public and private sectors. The Windows 10 refresh is expected to generate strongest growth in the midmarket as more of the larger accounts were fulfilled at the tail end of 2018. The outlook for desktops remains negative but has been modestly improved, primarily driven by small and ultrasmall form factors that provide an optimal solution to maximizing desk space without compromising on power.

"The Western European PC market is expected to remain constrained, driven by the CPU supply chain shortage and the difficult political situation in major economies," said Malini Paul, research manager, IDC Western European Personal Computing Devices. "While the ongoing shortage of notebooks is anticipated to ease by end of 2019Q2, the CPU supply issue with desktops will continue to impact shipments in the second half of the year."

With data being the most valuable resource for businesses, security will continue to be very important in the commercial space, as companies require devices that can be trusted. Consequently, newer models with enhanced security measures will continue to garner higher demand. The ongoing shift in consumer demand toward more thin and light mobile form factors continues to be a challenge for desktop adoption. However, with better prospects in gaming, strong processing power, and ability to customize, desktops will give the form factor greater relevance in the consumer category. Ultraslims, convertibles, and gaming will continue to drive the consumer space. In addition, the anticipated shift in the CPU shortage toward desktops in 2019H2 will contribute to the overall improvement of notebooks in the consumer market in 2019.

"The overall PC market results in the CEE and MEA regions were very different for 2018. CEE reported healthy growth of 6.5% YoY, whereas MEA contracted by 6.5% YoY. The CEE region was mostly driven by strong demand in Russia in both consumer and commercial sectors, while MEA was inhibited by the economic and political uncertainties and the currency fluctuation in Turkey," said Stefania Lorenz, associate VP, IDC CEMA.

"The outlook for MEA in 2019H1 will remain obscured by economic uncertainty and CPU shortages. However, the region is foreseeing a return to growth in the second half of 2019 as Turkey is expected to turn around after the worst market contraction ever witnessed in 2018H2. The CEE region is expected to slow down in 2019, after four years of continuous growth. The first quarter in 2019 will be affected by the Intel CPU shortage and some built-up inventory across the region, while the remaining quarters of the year are forecast to be flat with few visible deals in the pipeline," she said.

IDC's Quarterly PCD Tracker provides unmatched market coverage and forecasts for the entire device space, covering PCs and tablets, in more than 80 countries — providing fast, essential, and comprehensive market information across the entire personal computing device market.

Share on:

Suggested Items

Nanotechnology Market to Surpass $53.51 Billion by 2031

04/25/2024 | PRNewswireSkyQuest projects that the nanotechnology market will attain a value of USD 53.51 billion by 2031, with a CAGR of 36.4% over the forecast period (2024-2031).

Technica USA Presents Inaugural Supplier Alliance Award at IPC APEX EXPO 2024

04/24/2024 | Technica USADuring IPC APEX EXPO 2024, Technica USA took the opportunity to thank all of their supply partners that made the effort to join them for the exhibition in their booth, as well to all of our SMT partners that had their own booths, with the latest in automation and process technology.

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.