It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowChina's Power Semiconductor Market Posts 12% Growth

March 7, 2019 | TrendForceEstimated reading time: 2 minutes

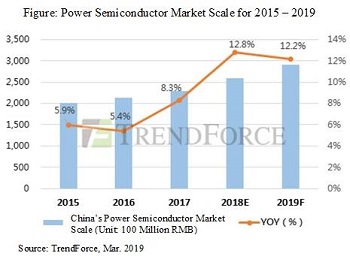

Global market research institute TrendForce points out in its latest Breakdown Analysis of China's Semiconductor Industry that, thanks to the large leap in demand of end markets such as those of new energy vehicles (NEVs) and industrial controls , as well as the stockouts and price hikes of several products such as MOSFET and IGBT, China's power semiconductor market has experienced a large growth of 12.76% to 259.1 billion RMB, with the discrete component market coming to a size of 187.4 billion RMB, a 14.7% increase from 2017; the power management IC (PMIC) market arrived at a size of 71.7 billion RMB, an 8% increase compared to 2017.

TrendForce analyst Royce Xie points out that power semiconductors still see an upward market trend in 2019 despite the trade dispute and other disadvantageous factors; it suffers less than other IC products do due to being driven by demand. TrendForce predicts that China's power semiconductor market will reach a size of 290.7 billion RMB in 2019, a 12.17% growth compared to 2018, maintaining double digit growth.

Thanks to China's policy of replacing foreign products with domestic ones and the stockout-induced rise in prices, many of China's homegrown power semiconductor suppliers have performed spectacularly and are further increasing in reach and pace. One such supplier is BYD Microelectronics, which rose speedily to stardom, acquiring a market share of over 20% in China's automotive IGBT market due to poessessing an end-product advantage, and broke into China's top three IGBT suppliers in sales amounts. MOSFET suppliers Sino-Microelectronics and Yangjie Technology enjoyed a large increase in revenue , and are gradually easing into the IGBT market.

In addition, suppliers planning and constructing IGBT production lines include Silan Microelectronics, who is constructing a 12-inch unique production line in Xiamen; China Resources Microelectronics, who is constructing a 12-inch unique production line in Chongqing; and GTA Semiconductor, who is working on its professional, automotive-grade IGBT production lines. Concurrently, several suppliers are also developing SiC and other new areas in materials technology, with BASiC Semiconductor already having mass produced and made available SiC MOSFETs. The foundry, Sanan Optoelectronics, has also opened up its SiC production lines for orders; BYD microelectronics has also successfully developed SiC MOSFETs, and will work towards a complete replacement of silicon-based IGBT with SiC MOSFETs by 2023.

Looking forwards at 2019 from an end-demand point of view, NEVs are still the largest source of demand in China's power semiconductor market. According to TrendForce's statistics, China is predicted to produce 1.5 million NEVs in 2019—a growth of 45% from the previous year—and the accompanying need for advanced driver assistance systems (ADAS), electrical controls and charging stations will bolster the market scale for power components by 27 billion RMB. At the same time, the base station equipment required to establish 5G connections and the speedy development of IoT and cloud computing (as a result of widespread 5G usage) will bring about a long-running high demand for power semiconductors. Furthermore, plans for industrial automation will continue their course, and related power supplies,controllers and drive circuits will continue to raise procurements of China's power semiconductors.

On the supply side, although there will be 3 to 5 power semiconductor lines entering mass production in 2019, predictions by TrendForce are pessimistic about the possibility of a significant recovery in the power component stockout for the first three quarters in 2019, and it is expected that several suppliers will continue to raise product prices. Considering the technological developments made by suppliers, SiC MOSFETs may further replace silicon-based IGBT in automotive sectors, while silicon-based IGBT may find developments in lower power, higher efficiency applications.

Share on:

Suggested Items

Technica USA Presents Inaugural Supplier Alliance Award at IPC APEX EXPO 2024

04/24/2024 | Technica USADuring IPC APEX EXPO 2024, Technica USA took the opportunity to thank all of their supply partners that made the effort to join them for the exhibition in their booth, as well to all of our SMT partners that had their own booths, with the latest in automation and process technology.

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.