The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryDRAM Capex to Plunge 28% in 2019 After Huge Outlays in 2017-18

July 11, 2019 | IC InsightsEstimated reading time: 1 minute

One of the significant questions facing the IC industry in the second half of 2019 is if and when the DRAM market will rebound. Any rebound in the market will be driven in part by available manufacturing capacity. After huge capex outlays for DRAM in 2017 and 2018, the question becomes how much new capacity will come online and how far DRAM prices (price per bit) will fall as a result of this buildup.

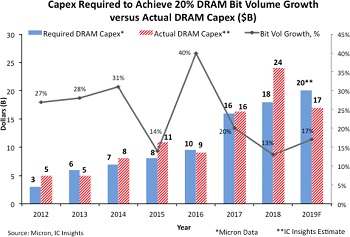

The three main DRAM suppliers—Samsung, SK Hynix, and Micron—generally agree that DRAM bit volume will grow roughly 20% per year over the next few years. The figure shows Micron’s perspective on the capex required to increase DRAM bit volume shipments 20% per year (data from Micron’s 2018 Analyst and Investor Event) versus IC Insights’ DRAM capex history and forecast data.

With new and very complex DRAM technologies requiring much more fab equipment and more fab space needed to house this equipment, Micron estimates that the industry capex required to grow DRAM bit volume by 20% more than doubled from $8 billion in 2015 to $18 billion in 2018! Actual DRAM expenditures in 2016 were slightly below what was needed to increase bit volume 20% and about equal to what was needed in 2017. However, in 2018, capex targeting the DRAM market reached $23.7 billion, 32% more than the $18.0 billion that was deemed necessary to grow DRAM bit volume by 20%. It is worth noting that in 2018, DRAM bit volume increased only 13% and is forecast to increase 17% in 2019.

Too much capex spending typically leads to overcapacity and subsequent pricing weakness—a condition that is amplified by economic weakness and softer demand from end-users. With Samsung, SK Hynix, and Micron aggressively spending to upgrade/add DRAM capacity last year, and with economic and trade uncertainties continuing to permeate global markets, IC Insights believes that the risk of too much DRAM capacity and the subsequent pricing weakness that results will continue for the remainder of 2019. On a brighter note, actual DRAM capex spending in 2019 is forecast to be less than what is required to maintain 20% bit volume growth. That could offset the overspending in 2018 and help start a return to supply-demand balance within the DRAM market in 2020.

Share on:

Suggested Items

KIC’s Miles Moreau to Present Profiling Basics and Best Practices at SMTA Wisconsin Chapter PCBA Profile Workshop

01/25/2024 | KICKIC, a renowned pioneer in thermal process and temperature measurement solutions for electronics manufacturing, announces that Miles Moreau, General Manager, will be a featured speaker at the SMTA Wisconsin Chapter In-Person PCBA Profile Workshop.

The Drive Toward UHDI and Substrates

09/20/2023 | I-Connect007 Editorial TeamPanasonic’s Darren Hitchcock spoke with the I-Connect007 Editorial Team on the complexities of moving toward ultra HDI manufacturing. As we learn in this conversation, the number of shifting constraints relative to traditional PCB fabrication is quite large and can sometimes conflict with each other.

Standard Of Excellence: The Products of the Future

09/19/2023 | Anaya Vardya -- Column: Standard of ExcellenceIn my last column, I discussed cutting-edge innovations in printed circuit board technology, focusing on innovative trends in ultra HDI, embedded passives and components, green PCBs, and advanced substrate materials. This month, I’m following up with the products these new PCB technologies are destined for. Why do we need all these new technologies?

Experience ViTrox's State-of-the-Art Offerings at SMTA Guadalajara 2023 Presented by Sales Channel Partner—SMTo Engineering

09/18/2023 | ViTroxViTrox, which aims to be the world’s most trusted technology company, is excited to announce that our trusted Sales Channel Partner (SCP) in Mexico, SMTo Engineering, S.A. de C.V., will be participating in SMTA Guadalajara Expo & Tech Forum. They will be exhibiting in Booth #911 from the 25th to the 26th of October 2023, at the Expo Guadalajara in Jalisco, Mexico.

Intel Unveils Industry-Leading Glass Substrates to Meet Demand for More Powerful Compute

09/18/2023 | IntelIntel announced one of the industry’s first glass substrates for next-generation advanced packaging, planned for the latter part of this decade.