It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowIndia Smartphone Market Registers Highest Q2 Shipments in 2Q19

August 13, 2019 | IDCEstimated reading time: 4 minutes

According to the International Data Corporation’s (IDC) Asia/Pacific Quarterly Mobile Phone Tracker, India smartphone market saw highest ever second quarter shipment of 36.9 million in 2Q19, with a 9.9% year-on-year (YoY) and 14.8% quarter-on-quarter (QoQ) growth. A total of 69.3 million mobile phones were shipped to India in 2Q19, which was up 7.6% over the previous quarter.

“Despite the efforts towards multi-channel retailing by almost all vendors, the online channel continued its growth momentum fueled by multiple new launches, attractive offers and affordability schemes like EMIs/cashbacks. This resulted in YoY growth of 12.4% for the online channel with an overall share of 36.8% in 2Q19,” says Upasana Joshi, Associate Research Manager, Client Devices, IDC India.

Offline channel registered an 8.5% YoY growth driven by the new launches in Samsung Galaxy A series, marketing activities by vivo during IPL (Indian cricket league) and Xiaomi’s growing multichannel distribution.

The overall market ASP stood at US$159 in 2Q19 with 78% of the market below US$200 price segment. However, the fastest growing segment was US$200-300 with 105.2% YoY growth. This was mainly due to the demand from customers looking to upgrade, additionally fueled by China-based brands which are bringing innovations and flagship like design language at mid-price segments.

Joshi further adds, “US$400-$600 was the second-fastest-growing segment with 16.3% YoY growth in 2Q19. OnePlus led this segment with a 63.6% share at the back of newly launched OnePlus 7 series. In the premium (US$500+) segment, Apple bettered Samsung for the leadership position with an overall share of 41.2% in 2Q19 as the iPhone XR demand saw an uplift after the price drop and aided by heavy promotional activities.

The feature phone market continued its decline with 32.4 million-unit shipments, registering a drop of 26.3% YoY in 2Q19. This was due to lower shipments of 4G-enabled feature phones with 40.3% YoY decline in 2Q19. The 2G feature phone segment also declined as challenges remain for Indian brands along with small players facing heat owing to duty hikes on imports.

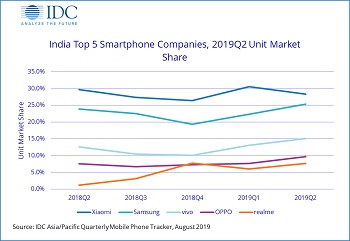

Top 5 Smartphone Vendor Highlights

Xiaomi saw its shipment volume grow by 4.8% YoY in 2Q19 with Redmi 6A and Redmi Note 7 Pro as the highest shipped models in the overall market. Xiaomi also maintained its dominance in the online channel with a market share of 46.5%, along with growing footprint in the offline channel which accounted for 39.5% of Xiaomi shipments in 2Q19.

Samsung registered a strong 16.6% YoY growth in 2Q19 fueled by newly launched Galaxy A series across low and mid-price segments. Galaxy A10 and A2 Core were amongst the top 5 models overall for the market. The vendor was also offering attractive channel schemes to clear the stocks of Galaxy J series. Galaxy M series (exclusive online till the end of 2Q19) saw price reductions which helped retain the 13.5% market share in the online channel in 2Q19 for Samsung.

vivo saw a strong YoY growth of 31.6% in 2Q19. Its affordable model Y91 featured in the top 5 model lists nationally. vivo also launched its first exclusive online model “Z1 Pro” priced aggressively in US$200-300 segment.

OPPO had a strong quarter with YoY growth of 41.0%, because of affordable A series - A3s and newly launched A1K and A5s. Online channel accounted for 19.1% for the vendor-driven by online exclusive model “K1”.

realme saw multifold growth YoY in 2Q19, driven by newly launched model C2 and 3/3Pro series. The vendor was second in the online channel with 16.5% market share in 2Q19, along with ongoing efforts for expansion in the offline channel which accounted for 21.0% of its shipments in 2Q19.

IDC India Forecast

Navkendar Singh, Research Director, Client Devices & IPDS, IDC India observes, “India smartphone market will continue its growth trajectory in the 2nd half 2019, but the consolidation of top few brands will continue. This will make it much more challenging for smaller players to find niches of growth. A very strong 2H19 is essential to bring double-digit YoY growth in the fastest-growing smartphone market of this size globally. We should expect continued aggression by the online heavy brands and eTailers in the next few months fueled by new launches and price reductions of last few launches, leading up to the festive season in October. We will also see a much more competitive offline market play going forward, with all the major brands fighting for limited shelf space, which will make the retail channel very critical for any brand’s success.”

About IDC Trackers

IDC Tracker products provide accurate and timely market size, company share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC's Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools. The IDC Tracker Charts app allows users to view data charts from the most recent IDC Tracker products on their iPhone and iPad.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a subsidiary of IDG, the world's leading technology media, research, and events company.

Share on:

Suggested Items

Orbex Secures £16.7m Investment for Rocket ‘Ramp Up’ Period

04/24/2024 | OrbexThe UK spaceflight company Orbex has received £16.7m from six backers in an update to its Series C funding round.

Real Time with... IPC APEX EXPO 2024: Going Vertical: SCHMID's Advanced Solutions for Printed Circuit Boards

04/24/2024 | Real Time with...IPC APEX EXPOEditor Marcy LaRont chats with Bob Ferguson, the president of SCHMID, about advanced solutions for PCBs and the equipment they are highlighting at this year's show. He delves into vertical no-touch handling systems and the prospect of achieving sub-10-micron lines. Inspired by SCHMID's technology, Bob expresses excitement about where the industry is today.

Real Time with... IPC APEX EXPO 2024: Advancements in Laser Depaneling with LPKF

04/24/2024 | Real Time with...IPC APEX EXPOJake Benz, LPKF sales manager for North America, discusses the company's advancements in laser depaneling. LPKF has introduced a green wavelength laser for processing rigid FR-4 circuit boards, bringing significant gains in processing speeds to market. The company transitioned from IR CO2 to UV wavelength due to heat and burning issues.

Adura Solutions Exhibits at Del Mar 2024

04/24/2024 | Adura SolutionsSumit Tomar, CEO of Adura Solutions, has announced that his company will be exhibiting at this year’s Del Mar Electronics and Manufacturing Show to be held at the Del Mar Fairgrounds, San Diego, California, April 24-25.

Winner of The Science Show Rakett 69 Receives Incap Scholarship

04/24/2024 | IncapThe winner of the Rakett 69 science show, Andri Türkson, who stood out as an electronics enthusiast, received a scholarship from Incap Estonia, along with an internship opportunity in Saaremaa.