The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryMiddle East & Africa PC Monitors Market Sees First Quarterly Growth Since 2017, but Outlook Remains Bleak

September 23, 2019 | IDCEstimated reading time: 4 minutes

The Middle East and Africa (MEA) PC monitors market saw shipments reach a value of $168.98 million for the second quarter of this year, according to the latest insights from International Data Corporation (IDC). The global technology research and consulting firm's Quarterly PC Monitors Tracker shows that a total of 1.1 million units were shipped across the region during Q2 2019, up 1.8% year on year (YoY).

“After suffering five sequential quarters of YoY declines, the positive growth seen in Q2 2019 offered some welcome relief for the MEA PC monitors market,” says Nourhan Abdullah, a senior research analyst at IDC. “The growth was primarily spurred by the performance of the markets in Turkey and South Africa, where monitor shipments increased 18.5% and 8.0% YoY, respectively, in Q2 2019. Turkey, the region’s largest market, finally saw a stabilization of its currency after experiencing many quarters of uncertainty and fluctuations, while South Africa has started to recover from the tough recession that has been hanging over the country since 2017.”

Commercial demand accounted for 75.1% of the market in Q2 2019, with shipments to this segment increasing 4.1% YoY. The consumer segment, which accounts for the remaining 24.9% of the region’s market, saw shipments decline 4.6% YoY as currency fluctuations and the introduction of VAT in many MEA markets have made products more expensive for end consumers.

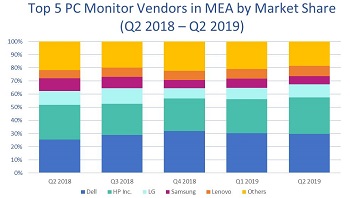

Top Five Vendors

- Dell: Dell remained in first place in Q2 2019 with 29.8% share of the overall MEA market. The vendor shipped 329,000 units to the region, up 19.9% YoY.

- HP Inc.: Second-placed HP Inc. is closing in on Dell with 27.8% market share. The vendor shipped 306,000 units in Q2 2019, representing a YoY increase of 7.0%.

- LG: Third-ranked LG is the largest consumer-oriented brand in the MEA market. The vendor’s overall shipments declined 5.9% YoY to 108,000 units in Q2 2019, accounting for 9.8% of the market.

- Lenovo: Fourth-placed Lenovo posted YoY of 23.4% in Q2 2019, courtesy of its strong performance in governmental deals. The vendor shipped 85,000 units for the quarter, which equates to 7.7% share.

- Samsung: Samsung remained in fifth place with 6.2% share after seeing its shipments decline 33% YoY to 68,000 units.

Technology Highlights

- Screen Sizes: Widescreen monitors now account for 98.6% of the market. 21.5” screens lead the way with 21.5% share, followed by 23.8” (18.7%) and 18.5” (16.9%).

- Gaming: Shipments of gaming monitors increased 62.5% YoY in Q2 2019. This trend is fueling growing demand for larger screen sizes, particularly 21.5”, 24”, and 27” monitors. The top three brands in this space – Samsung, LG, and Dell – accounted for 62.8% share of the MEA gaming market in Q2 2019.

- Curved Monitors: Despite their relatively high prices, shipments of curved monitors across the MEA region increased 49.3% YoY in Q2 2019. However, this remains a very niche segment of the market, accounting for just 5.1% of overall shipments for the quarter.

Looking ahead, IDC projects the MEA PC monitors market will remain stable through the end of 2019 with 4.2 million units to be shipped for the year as a whole. “This translates into YoY growth of 0.1%, and while that doesn’t sound particularly encouraging, it represents a huge improvement on the 11.6% YoY decline seen in 2018,” says Abdullah. “This is being caused by the growth and stabilization of the region’s largest markets and should therefore not be construed as an overall shift in the long-term trend of the market.”

The long-term outlook is not too positive for the MEA PC monitors market, with IDC forecasting shipments to decline at a five-year compound annual growth rate (CAGR) of 3.1% through to the end of 2023. "This decline will be caused by consumers increasingly choosing to spend their hard-earned disposable income on other technologies, such as smartphones, laptops, and tablets," says Nabila Popal, a senior research manager at IDC. "Vendors should focus on growing their presence in niche sectors like gaming monitors to grow within the consumer segment and focus on commercial pipelines in order to remain relevant in this declining industry."

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC's Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools. The IDC Tracker Charts app allows users to view data charts from the most recent IDC Tracker products on their iPhone and iPad. The IDC Tracker Chart app is also available for Android Phones and Android Tablets.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a subsidiary of IDG, the world's leading technology media, research, and events company.

Share on:

Suggested Items

Warm Windows and Streamlined Skin Patches – IDTechEx Explores Flexible and Printed Electronics

04/26/2024 | IDTechExFlexible and printed electronics can be integrated into cars and homes to create modern aesthetics that are beneficial and easy to use. From luminous car controls to food labels that communicate the quality of food, the uses of this technology are endless and can upgrade many areas of everyday life.

iNEMI Packaging Tech Topic Series: Role of EDA in Advanced Semiconductor Packaging

04/26/2024 | iNEMIAdvanced semiconductor packaging with heterogenous integration has made on-package integration of multiple chips a crucial part of finding alternatives to transistor scaling. Historically, EDA tools for front-end and back-end design have evolved separately; however, design complexity and the increased number of die-to-die or die-to-substrate interconnections has led to the need for EDA tools that can support integration of overall design planning, implementation, and system analysis in a single cockpit.

Koh Young Showcases Award-winning Inspection Solutions at SMTconnect with SmartRep in Hall 4A.225

04/25/2024 | Koh Young TechnologyKoh Young Technology, the industry leader in True 3D measurement-based inspection solutions, will showcase an array of award-winning inspection and measurement solutions at SMTconnect alongside its sales partner, SmartRep, in booth 4A.225 at NürnbergMesse from June 11-13, 2023. The following offers a glimpse into what Koh Young will present at the tradeshow:

Real Time with… IPC APEX EXPO 2024: Plasmatreat: Innovative Surface Preparation Solutions

04/25/2024 | Real Time with...IPC APEX EXPOIn this interview, Editor Nolan Johnson speaks with Hardev Grewal, CEO and president of Plasmatreat, a developer of atmospheric plasma solutions. Plasmatreat uses clean compressed air and electricity to create plasma, offering environmentally friendly methods for surface preparation. Their technology measures plasma density for process optimization and can remove organic micro-contamination. Nolan and Hardev also discuss REDOX-Tool, a new technology for removing metal oxides.

Nanotechnology Market to Surpass $53.51 Billion by 2031

04/25/2024 | PRNewswireSkyQuest projects that the nanotechnology market will attain a value of USD 53.51 billion by 2031, with a CAGR of 36.4% over the forecast period (2024-2031).