The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryShipments of Monitor Panels are Projected to Show YoY Decline of 8.8% for 2022

January 2, 2023 | TrendForceEstimated reading time: 1 minute

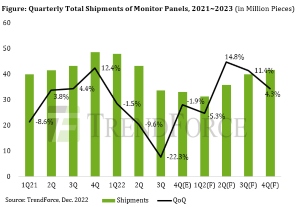

Shipments of monitor panels have fallen over the quarters this year due to various factors that have caused disruptions across the global economy and politics. TrendForce projects that shipments of monitor panels will total just around 158 million pieces for 2022, showing a YoY decline of 8.8%.

According to TrendForce’s research on the market for display panels, monitor panels experienced a large downward shipment correction later than did TV and NB panels. For TV panels, the correction phase began in 3Q21. Turning to NB panels, a steep decline in shipments occurred in 2Q22. As for monitor panels, their shipments had not fallen significantly until 3Q22. With the correction taking place at a later time, the eventual rebound will also occur at a more distant time in the future. Since monitor brands are still holding an excessively high level of panel inventory at this moment, shipments of monitor panels are forecasted to drop again by 5.3% QoQ for 1Q23.

Looking further ahead to 2Q23, inventory level will return to a more optimal level for brands and channels. With the impending arrival of the traditional peak season in 2H23, shipments of monitor panels are forecasted to rebound to around 35.7 million units for 2Q22 and thereby return to the average level for second-quarter shipments in the four years before the emergence of the COVID-19 pandemic (i.e., from 2016 to 2019). Also, since the shipment figure for 1Q23 will be a low base for comparison, the shipment figure for 2Q23 will reflect a double-digit QoQ growth. Moving into 2H23, global inflation is expected to ease, and China’s economy is anticipated to undergo a recovery due to the loosening of pandemic-related restrictions. Therefore, the supply-demand dynamics of the market for monitor panels will likely follow the usual seasonal patterns.

Based on TrendForce’s tracking of panel shipments, shipments of monitor panels started to slide after reaching a peak in 4Q21 and are expected to arrive at a trough in 1Q23. After inventory level returns to an optimal level for the entire supply chain, brands will regain procurement momentum. Then, shipments of monitor panels will climb over the quarters. TrendForce currently forecasts that the total for 2023 will come to 149 million pieces, showing a diminished YoY growth rate of 5.8%.

Share on:

Suggested Items

NCAB Group Posts Interim Report Q1 2024

04/26/2024 | NCAB GroupNet sales decreased by 17% to SEK 950.6 million (1,146.4). Compared with the year-earlier period, sales were affected bylower prices and continued inventory adjustments by customers. In USD, net sales decreased 17%. For comparable units, net sales decreased 24% in both SEK and USD.

Rogers Corporation Reports Q1 2024 Results

04/26/2024 | Rogers CorporationNet sales of $213.4 million increased 4.3% versus the prior quarter resulting from higher sales in the AES and EMS business units. AES net sales increased by 4.1% primarily related to higher aerospace and defense (A&D), wireless infrastructure, industrial and renewable energy sales, partially offset by lower EV/HEV and ADAS sales. EMS net sales increased by 2.8% primarily from higher general industrial, A&D and EV/HEV sales, partially offset by seasonally lower portable electronics sales.

NOTE Releases Interim Report for January-March 2024.

04/23/2024 | NOTENOTE has announced its interim report for January-March 2024.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.

Aspocomp’s Q1 Net Sales and Operating Result Decreased YoY

04/18/2024 | AspocompInflation and interest rates, weak economic development, the uncertainties posed by Russia’s war of aggression and the situation in the Middle East, and global trade policy tensions will affect the operating environment of Aspocomp and its customers in the 2024 fiscal year.