Happy’s Tech Talk #41: Sustainability and Circularity for Electronics Manufacturing

Happy’s Tech Talk #41: Sustainability and Circularity for Electronics Manufacturing Facing the Future: Challenges and Opportunities in Reshoring PCB Manufacturing

Facing the Future: Challenges and Opportunities in Reshoring PCB Manufacturing It’s Only Common Sense: Stop Chasing New Customers and Start Keeping the Ones You Have

It’s Only Common Sense: Stop Chasing New Customers and Start Keeping the Ones You Have

LCD Monitor Panel Output Predicted to Increase 15% QoQ in 2Q23

March 31, 2023 | TrendForceEstimated reading time: 1 minute

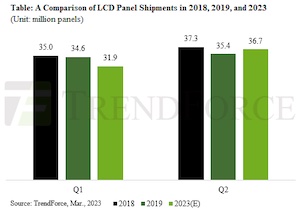

TrendForce estimates that approximately 31.9 million LCD monitor panels were shipped in 1Q23, indicating a 2.6% QoQ and 33.4% YoY decline. This drop in shipments can be attributed to several factors, including fewer working days, weak demand in the end-market, and inventory adjustments. However, since March, brands have been more optimistic about product demand for 2Q23, which has driven up order visibility for LCD monitor panels. TrendForce projects that shipments will reach 36.7 million units in 2Q23—a 15.1% QoQ growth. Comparing this number to pre-pandemic figures, with 37.3 million shipments in 2Q18 and 35.4 million shipments in 2Q19, we can see that the figures are almost on par.

TrendForce explains that there are three main factors contributing to the increase in shipment levels in 2Q23: Firstly, Internet cafés in China are seeing a rising surge of customers after COVID restrictions were lifted in December of last year. To help attract these customers, cafés are working to upgrade their current gaming LCD monitors to higher-end models. However, the current supply of ICs (DDICs and T-cons) used in the production of these high-end gaming monitors may be insufficient in fulfilling this sudden uptick in demand.

Secondly, panel makers have observed that demand from international logistics channels is on the rise as channels are working to replenish their inventories after destocking for several quarters. Lastly, while monitor brands were forced to contend with a frozen consumer market in 2022, they are now stocking up in preparation for China’s 618 Shopping Day, which is expected to revitalize sales as China relaxes its COVID restrictions in an effort to restore its economy. Additionally, brands are being enticed by low panel prices to stock up.

TrendForce believes that demand recovery in 2Q23 will primarily be boosted by consumers, while commercial demand continues to remain sluggish; we can expect in 2H23 for brands to continue maintaining a conservative outlook on commercial demand. Meanwhile, as we move into the traditionally peak final half of the year, judging on how successful sales are during China’s 618 Shopping Day and in European markets, there may be further opportunities for consumer markets to boost demand.

Share on:

Testimonial

"We’re proud to call I-Connect007 a trusted partner. Their innovative approach and industry insight made our podcast collaboration a success by connecting us with the right audience and delivering real results."

Julia McCaffrey - NCAB GroupSuggested Items

Amidst U.S. Strategy Shift, Foxconn Sells Lordstown, Ohio Plant for $88 Million

08/07/2025 | I-Connect007 Editorial TeamAs part of a strategic shift in its US operations, Taiwan-based Foxconn (Hon Hai Precision Industry’s) subsidiaries are selling off assets at its Lordstown, Ohio, facility, the company announced on Aug. 4.

Element Solutions Inc Reports Strong Growth in Second Quarter 2025 Financial Results

08/01/2025 | Element Solutions Inc.Element Solutions Inc, a global and diversified specialty chemicals company, today announced its financial results for the three and six months ended June 30, 2025.

Thanks a Million: STI Electronics Celebrates Creating 1 Million Power Supply Boards for Night Vision Goggles

07/28/2025 | Sandy Gentry, Community MagazineIn an industry where precision and reliability are paramount, STI Electronics Inc. recently celebrated a remarkable milestone: the production of its 1 millionth power supply board for L3Harris Technologies’ state-of-the-art night vision goggles. This achievement not only marks a significant volume for military electronics manufacturing but also highlights the enduring partnership between STI and L3Harris.

Inside Aimtron’s Cross-border EMS Strategy

07/08/2025 | Nolan Johnson, SMT007 MagazineMukesh Vasani immigrated from a very small farming village in India to the U.S. in 1995 as a civil engineer. After shifting into electronics, Mukesh built his Chicago-based company, Aimtron, into a successful enterprise by combining quality with competitive pricing. He leveraged his roots in India to expand manufacturing without compromising on quality.

Tariff Effects and China Subsidies Soften 1Q25 Downturn; Foundry Revenue Decline Narrows to 5.4%

06/09/2025 | TrendForceTrendForce’s latest investigations find that the global foundry industry recorded 1Q25 revenue of US$36.4 billion—a 5.4% QoQ decline. The downturn was softened by last-minute rush orders from clients ahead of the U.S. reciprocal tariff exemption deadline, as well as continued momentum from China’s 2024 consumer subsidy program.