Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024

It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024 Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowSemiconductor Manufacturing Monitor Points to Moderating Industry Contraction in Q2 2023

May 16, 2023 | SEMIEstimated reading time: 1 minute

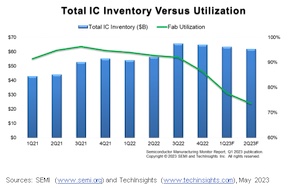

The current global semiconductor manufacturing industry contraction is expected to moderate in the second quarter of 2023 and give way to a gradual recovery starting in the third quarter, SEMI announced in its Q1 2023 publication of the Semiconductor Manufacturing Monitor (SMM) Report, prepared in partnership with TechInsights.

In the second quarter of 2023, industry indicators including IC sales and silicon shipments – both partly supported by seasonality – point to quarter-over-quarter improvements. However, despite the gains, elevated inventories continue to dampen silicon shipments and fab utilization rates remain significantly lower than levels registered last year. In addition, semiconductor equipment sales continue to decline in parallel with capital expenditure adjustments by major industry stakeholders.

The indicators point to a likely bottoming of the current downturn in the second quarter of 2023 with a slow recovery expected to begin in the year’s second half.

“The current market downturn is compounded by soft consumer demand and elevated inventory levels and has led to a sharp decline in semiconductor fab utilization,” said Clark Tseng, Senior Director of Market Intelligence at SEMI. “However, as the inventory correction comes to an end in mid-2023, a mild recovery is expected in the second half of the year driven by a pickup in demand for inventory and the holiday season.”

“Despite ongoing uncertainties and risks, we expect continuing production cuts and capex reductions, especially in the memory market, will start having a positive impact on market fundamentals in the latter part of the year, resulting in a more balanced market environment,” said Risto Puhakka, VP of Market Analysis at TechInsights.

The Semiconductor Manufacturing Monitor (SMM) report provides end-to-end data on the worldwide semiconductor manufacturing industry. The report highlights key trends based on industry indicators including capital equipment, fab capacity, and semiconductor and electronics sales, and includes a capital equipment market forecast. The SMM report also contains two years of quarterly data and a one-quarter outlook for the semiconductor manufacturing supply chain including leading IDM, fabless, foundry, and OSAT companies. An SMM subscription includes quarterly reports.

Share on:

Suggested Items

I-Connect007 Editor’s Choice: Five Must-Reads for the Week

04/19/2024 | Marcy LaRont, PCB007 MagazineFor my must-read picks of the week, I’m highlighting Parker Capers, a young professional seeking employment, solid counsel from Dan Beaulieu on what your post-show plan should look like, more information and insight on “chiplets” and the need for secure data transfer standards from columnist Preeya Kuray, as well as Matt Stevenson’s design for reality wisdom. It’s a reminder to download one of our newest books (there are several) you don't want to miss if you are an assembler.

Absolute EMS Champions Collaboration Between Humans and Robots in Modern Manufacturing

04/19/2024 | Absolute EMS, Inc.Absolute EMS, Inc., an award-winning EMS provider of turnkey contract manufacturing services, offers a perfect factory environment that seamlessly blends robotic automation with human expertise.

ZESTRON Welcomes Whitlock Associates as New Addition to their Existing Rep Team in Florida

04/19/2024 | ZESTRONZESTRON, the leading global provider of high-precision cleaning products, services, and training solutions in the electronics manufacturing and semiconductor industries, is thrilled to announce the addition of Whitlock Associates to its esteemed network of sales representatives.

SEMI Applauds U.S. Chips Act Award for Samsung Electronics Facilities to Strengthen Domestic Semiconductor Supply Chain

04/17/2024 | SEMISEMI, the industry association serving the global electronics design and manufacturing supply chain, applauded the United States Department of Commerce’s announcement of a Preliminary Memorandum of Terms for an award under the CHIPS and Science Act to support the expansion of Samsung Electronics’ presence in Texas and the company’s development and production of leading-edge chips.

Ark Electronics Expands Global Manufacturing Factory Network in North America and Europe

04/17/2024 | PRNewswireElectronic Manufacturing Company Ark Electronics recently announced the expansion of its Global Factory Network with the addition of Electronics Manufacturing Service (EMS) capabilities in Mexico and Europe.