The Right Approach: I Hear the Train A Comin'

The Right Approach: I Hear the Train A Comin' It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing IndustryAsia/Pacific Semiconductor Fabless Market Size Decline 6.5% YoY in 2022, Expected Steady Growth in 2024

May 17, 2023 | IDCEstimated reading time: 2 minutes

According to the IDC Worldwide Semiconductor Technology Supply Chain Intelligence: IDMs, Fabless, Foundry, OSAT and Materials, factors including the Ukraine-Russia war, Chinese lockdowns, high inflationary pressures, and demand fluctuations resulted in the Asia/Pacific region’s semiconductor fabless market losing growth momentum in 2022 and an end to the trend of rising Integrated Circuit (IC) prices. The region’s semiconductor fabless market size in 2022 was US$78.5 billion, a decline of 6.5% compared to 2021 which marks the first year-on-year negative growth performance since the onset of the pandemic.

The global semiconductor industry experienced a sharp decline in 2022 after seeing growth in 2020 and 2021. Demand for consumer electronics including smartphones, laptops, tablets, TVs, and monitors plummeted while supply chain inventory levels increased. Short-term supply began exceeding demand, forcing companies to slow down the pace of expansion.

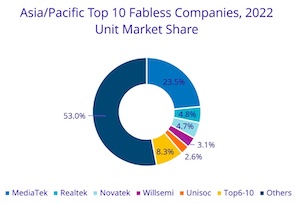

“The annual growth rate of the top 10 companies in Asia/Pacific was -5.1%, which was better than the overall market performance. From the perspective of regional momentum, Taiwan leads with 73% market share, while China and South Korea holds 22% and 5% market share respectively. Having the highest market share, Taiwan is considered to have a wide and deep influence on the region’s fabless market,” said Galen Zeng, Senior Research Manager, Semiconductor Research, IDC Asia/Pacific.

Among the top 10 semiconductor technology vendors are Taiwan’s MediaTek, Realtek, Novatek, and Himax; China’s Willsemi, Unisoc, HiSilicon, GigaDevice, and Bitmain; and South Korea’s LX Semicon. MediaTek plays an influential role with a market share of nearly 50% among the top 10 companies. The growth of MediaTek played a leading role by helping make up for the shortfalls of other Taiwanese firms, resulting in a 2% increase in Taiwan’s semiconductor fabless market share in the region compared to 2021. Chinese companies were affected by the overall unfavorable environment in China and saw their market share decline by 2%, while South Korea’s market share did not experience any major changes.

As for the outlook for 2023, although products such as display driver ICs and touch and display driver ICs were the first to enter a down cycle, these are now seeing the light of day with several products starting to see urgent orders and the need for inventory replenishment. The market demand for most semiconductor ICs remains depressed and the market size outlook remains sluggish. During the high base period in the first half of 2022, it was anticipated that the region’s fabless market size in the first half of 2023 would decrease by over 20% year-on-year, supply chains would continue to actively control inventory, and fabless companies would maintain low wafer production volumes at foundries. During the second half of 2023, it is expected that inventory will return to a healthy level, and that demand will also slowly recover. IDC forecasts that the Asia/Pacific region’s semiconductor fabless market size will decline by 19.1% year-on-year in 2023. It also predicts that it will progressively show stable and steady growth in 2024 as companies gradually shift products to applications including AI, high-performance computing, servers, data centers, automotive electronics, and industrial electronics to diversify operational risks.

This IDC research, Worldwide Semiconductor Technology Supply Chain Intelligence: IDMs, Fabless, Foundry, OSAT and Materials, provides holistic analysis of the worldwide semiconductor supply chain industry. The program delivers comprehensive insights across supply chain including materials, Fabless, OSAT, and semiconductor equipment. It covers the analysis of market dynamics, market competition, and key vendors' activities and the strategy plans to understand the key trends and factors impacting the market as it transitions to the new world of digital competition under geopolitical impact across countries and companies.

Share on:

Suggested Items

Nanotechnology Market to Surpass $53.51 Billion by 2031

04/25/2024 | PRNewswireSkyQuest projects that the nanotechnology market will attain a value of USD 53.51 billion by 2031, with a CAGR of 36.4% over the forecast period (2024-2031).

Technica USA Presents Inaugural Supplier Alliance Award at IPC APEX EXPO 2024

04/24/2024 | Technica USADuring IPC APEX EXPO 2024, Technica USA took the opportunity to thank all of their supply partners that made the effort to join them for the exhibition in their booth, as well to all of our SMT partners that had their own booths, with the latest in automation and process technology.

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.