Facing the Future: Challenges and Opportunities in Reshoring PCB Manufacturing

Facing the Future: Challenges and Opportunities in Reshoring PCB Manufacturing It’s Only Common Sense: Stop Chasing New Customers and Start Keeping the Ones You Have

It’s Only Common Sense: Stop Chasing New Customers and Start Keeping the Ones You Have Driving Innovation: Inner Layer Alignment Methods in PCB Production

Driving Innovation: Inner Layer Alignment Methods in PCB Production

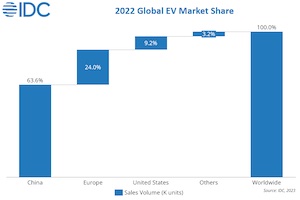

Global Electronic Vehicle Market Almost Reached 11M Units in 2022

May 26, 2023 | IDCEstimated reading time: 2 minutes

In a recent report from IDC’s Worldwide Semiconductor Automotive Ecosystem and Supply Chain, IDC provides an illustrative overview of the current industry dynamics and competition landscape of the global Electronic Vehicles (EV) market. With the trend of electrification, connection, autonomous driving, and sharing in the automobile industry, we see the EV market growing fast. In 2022, the worldwide EV market reached almost 11M units, with a penetration rate of 14%. Driven by improved supply, high oil prices, government subsidies, and price-guaranteed promotions by car companies, China’s electronic vehicle market reached almost 7M units with a penetration rate of 31.3% in 2022.

“Top performers have bigger market share,” says Adela Guo, Research Director, Automotive Semiconductor Research, IDC Asia Pacific.

The top 3 players worldwide, BYD, Tesla, and SAIC-GM Wuling, occupy 36.11% of the market in 2022. While in China the top 3 players, BYD, SAIC, and Tesla occupy 53% of the market in 2022. In the China EV market, the top 10 players are dominated by local brands except for Tesla in the third position with a market share of 10.3% in 2022.

IDC’s Advice for OEMs:

Target market: Continue investments in the most valuable markets, China, Europe, and North America which are competitive and valuable markets. Some developing countries also have potential such as Thailand, Philippines, Indonesia, etc.

Cooperate positioning: Automobile enterprises should start from their goals and positioning, then choose the right development path. Leading companies are positioned as energy companies or technology companies, which are bigger than automotive, while maximizing synergies between different business portfolios.

Technology strategy: OEMs need to choose the most suitable technological route, such as low cost, time to market and superior product. Increase investment in research and development to enhance their research and development capabilities, especially for software.

Supply chain strategy: To create a high tenacity supply chain, automotive companies need to consider changing their original pure outsourcing strategy and more actively arranging upstream core components from a strategic perspective, such as investment, cooperation, self-development to enhance the control and discourse power of the industrial chain. At the same time, build a more digital and intelligent supply chain management system to increase resilience and agility.

Talent strategy: OEMs should start as early as possible to discover their talent shortages, especially for internet and communication functions, enlarge their talent pool, try to attract global talent, at the same time, build health and attractive systems to attract top talent and maintain employee satisfaction.

“The industry transition will be fast, both opportunities and challenges exist. Only by establishing advantage in advance, can the players get ahead of their competitors and win the final victory,” ends Guo.

Share on:

Testimonial

"In a year when every marketing dollar mattered, I chose to keep I-Connect007 in our 2025 plan. Their commitment to high-quality, insightful content aligns with Koh Young’s values and helps readers navigate a changing industry. "

Brent Fischthal - Koh YoungSuggested Items

Insulectro and Electroninks Sign North American Distribution Agreement

08/12/2025 | InsulectroElectroninks, a leader in metal organic decomposition (MOD) inks for additive manufacturing and advanced semiconductor packaging, today announced a strategic collaboration and distribution partnership with Insulectro, a premier distributor of materials used in printed electronics and advanced interconnect manufacturing.

Global Excellence in PCB Design: The Global Electronics Association Expands to Italy

08/07/2025 | Global Electronics AssociationIn today's rapidly evolving electronics industry, printed circuit boards (PCBs) serve as the critical backbone influencing the success, reliability, and time-to-market of countless products. Recognizing this essential role, the Global Electronics Association (formerly IPC), a worldwide leader in electronics standards, certification, and education, is now expanding its internationally acclaimed PCB design training to Italy.

Inside the AI Hardware Boom: Servers, Substrates and Advanced Packaging

08/07/2025 | Edy Yu, Printed Circuit Information, China, and Marcy LaRont, I-Connect007AI is rewriting the hardware playbook, marrying complex software and algorithms to run and improve machine and equipment operations. Sorting through, managing, and utilizing massive amounts of data takes tremendous data storage and processing power. Enter the new generation of supercomputers and data servers. The data servers being built today are not your momma’s server, as they say.

It’s Only Common Sense: Sales as a Team Sport

08/04/2025 | Dan Beaulieu -- Column: It's Only Common SenseAnyone who has played, or even watched, sports knows that it’s not just about scoring points or making big plays—it’s about everyone working together toward a common goal. Sales is no different. Too often, sales is considered an individual activity, with each salesperson striving to hit his or her targets. However, the reality is that sales works best when it’s treated as a team sport, with everyone working toward a common goal.

Nordson Corporation Announces Earnings Release and Webcast for Third Quarter Fiscal Year 2025

07/31/2025 | Nordson CorporationNordson Corporation today announced it will release third quarter fiscal year 2025 earnings on August 20, 2025, after the close of the market.