It’s Only Common Sense: OCCAM—the Time Is Now

It’s Only Common Sense: OCCAM—the Time Is Now Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowTrendForce Trims LCD Monitor and Notebook Shipment Forecasts for Q2, Q3

July 6, 2015 | TrendForceEstimated reading time: 2 minutes

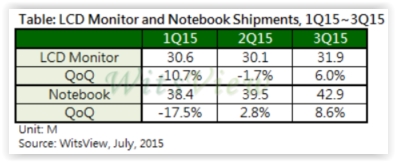

WitsView, a division of TrendForce, has made downward revisions to shipment forecasts of monitors and notebooks for this year’s second and third quarters according to its latest research. The revision is based on the depreciation of the euro and the emerging markets’ currencies as well as other factors.

According to WitsView’s Research Manager Anita Wang, the sharp depreciation of the euro has depressed the market demand for LCD monitors during the entire second quarter. The channel retailers are unwilling to stock up because they are not clearing their inventories quickly enough. Under this cycle of inventory accumulation and dropping demand, the projected monitor shipments for the second quarter will not grow but rather shrink by 1~2% quarterly, reaching 30.1M units shipped. The main goals of branded monitor vendors in the second quarter were to adjust their product mixes and help channel retailers get rid of excess inventories. Vendors are hoping demands will pick up in this year’s second half, when the overall inventory level in the channels is returning to normal. By that time retailers will stock up more product models carrying low-cost panels in preparation of annual sales events, which are important to vendors’ shipment targets.

“The base period for the second quarter shipments is relatively short,” Wang added. “This will spur monitor vendors to work harder to reach their annual shipment targets and spur stock-up demands in the channels.” The third quarter shipments are therefore likely to see a growth of 5~7% with 31.9M units shipped. This estimated shipment figure, however, also represents a 4.8% year-on-year decline.

Notebook market struggles as peak season sales did not reach expectations

WitsView has also revised the estimated shipments of notebooks for the second quarter downward from a quarterly growth of 8~9% to 2~4%, arriving at 39.5M units shipped. Traditionally, this is the period when branded notebook vendors launch their new models and retailers stock up for the back-to-school sales. However, the notebook market like the monitor market is badly affected by the depreciation of the euro and the emerging markets’ currencies. Hence, the notebook sales have fallen short of expectations. Vendors moreover have stocked up too many panels as they have maintained the same procurement volumes respectively. On the whole, the gradual recovery of the North American market is unlikely to offset the losses in Europe.

The notebook market appears to be uncharacteristically conservative as it enters the third quarter, which is the peak season for IT products. Even though Windows 10 is set to launch at the end of July, the news has not lifted the notebook market demand because the current Windows 7 and above users can get a free upgrade. In order to make the annual shipment quotas, notebook vendors are relying on the next-generation, Windows 10 notebooks that also carry the new Intel Skylake processors. They are also aggressively promoting the older models to prop up sales figures. With the notebook shipments performing below expectation in the second quarter, WitsView estimates the quarterly growth in the third quarter will reach 7~9%, down from the original projection of 12~13%. There is also an adjustment in the projected year-on-year decline for the period, from the original 0.2% to the revised 6.4%. As for the expected notebook shipment volume, about 42.9M units will be shipped in third quarter.

Share on:

Suggested Items

Technica USA Presents Inaugural Supplier Alliance Award at IPC APEX EXPO 2024

04/24/2024 | Technica USADuring IPC APEX EXPO 2024, Technica USA took the opportunity to thank all of their supply partners that made the effort to join them for the exhibition in their booth, as well to all of our SMT partners that had their own booths, with the latest in automation and process technology.

IDTechEx Report Unveils 3D Electronics Status and Opportunities

04/22/2024 | PRNewswire3D electronics is an emerging manufacturing approach that enables electronics to be integrated within or onto the surface of objects. 3D electronic manufacturing techniques empower new features, including mass customizability, greater integration, and improved sustainability in the electronics industry.

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.